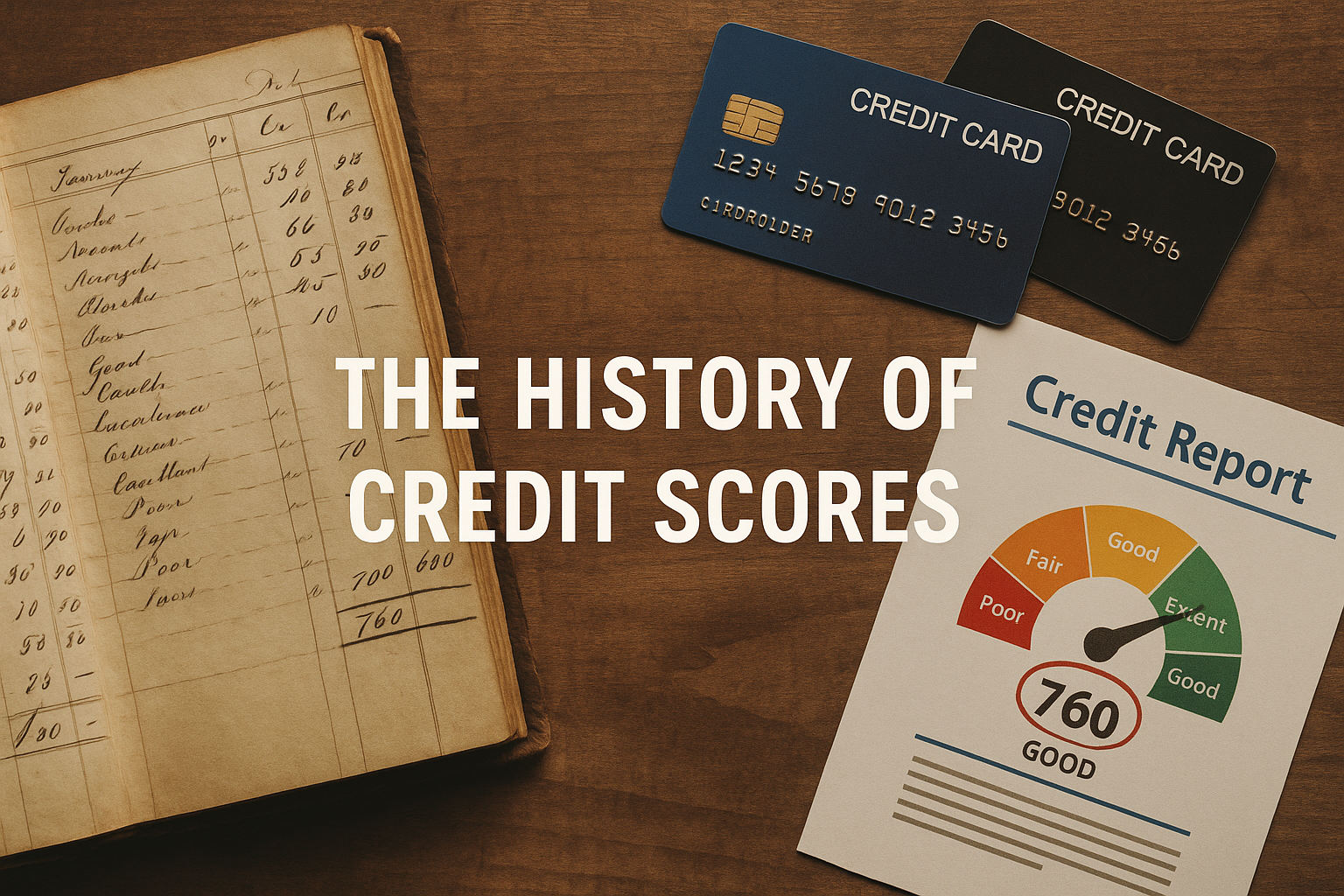

The Sketchy History Of The Credit Score

The Wild Origins of Credit Reporting

Modern credit bureaus like Equifax and Experian may seem sleek and data-driven now, but back in the day, they were more like neighborhood gossip clubs.

The roots of credit reporting trace all the way back to the 1700s in London, with a group called the Society of Guardians for the Protection of Trade Against Swindlers and Sharpers. (Yes, that’s a mouthful.) Their reports were more than just financial facts—they included juicy tidbits about customers’ personal lives.

This tradition carried over to 19th-century America, where local merchants formed small credit bureaus to share information about who was reliable and who wasn’t. They didn’t stop at your payment history. They’d dig into your personal life, checking on your marital status, drinking habits, and even what your neighbors thought of you. Privacy? Not even a concept back then.

Credit Reports Today

These days, credit reports have a slightly more professional vibe. They focus on things like:

- Your credit accounts (current and past)

- Payment history

- Balances and credit limits

- Personal identifiers like your Social Security number

Lenders use this data to figure out how risky it is to lend you money. Your credit score? That’s just a boiled-down version of all this info into a single number that decides your financial fate.

But let’s not forget: in the early days, credit reporting was basically a free-for-all. Agencies gathered everything they could and shared it with whoever wanted to know. You couldn’t access your own file or correct errors—it was all a big secret club, and you weren’t invited.

Modernizing the Chaos

By the 1960s, these small, local agencies started merging into larger networks. The credit bureaus were growing up—sort of. Congress finally stepped in with the Fair Credit Reporting Act (FCRA) in 1971. This law was a huge deal. For the first time, consumers got rights:

- You could see your credit file.

- You could dispute inaccurate info.

- Outdated info (usually over 7–10 years old) had to go.

- Lenders needed your permission to check your credit in certain situations.

This cleaned up some of the chaos, but let’s be real—it didn’t make the system perfect. The Big Three credit bureaus we know today—Experian, TransUnion, and Equifax—still had plenty of growing pains (and scandals).

The Big Three: A Quick Rundown

Here’s how the major players took over the credit game:

Equifax: Started in 1898 by a grocer selling lists of trustworthy customers. By the 1960s, it was collecting outrageous amounts of personal data and selling it to anyone who asked. After congressional hearings in the ‘70s, they rebranded as Equifax. Spoiler alert: The scandals didn’t stop there.

Experian: Originally formed in England in the 1820s as a merchant’s debt-sharing group. Experian went through a series of acquisitions and controversies, including lawsuits and data breaches, to become one of the Big Three.

TransUnion: This one began in the 1960s as a railcar leasing company. They bought up regional credit bureaus and joined the ranks of the big players. Like the others, they’ve had their share of lawsuits and consumer complaints.

Oh, and don’t forget the 2017 Equifax breach that exposed the personal data of 147 million people. Or Experian’s habit of scamming people with “free” credit reports that weren’t actually free. Or TransUnion’s website redirecting users to malware.

Why the Credit System Still Feels Rigged

Even with modernization, the credit system has its issues. For starters, it’s still unfair to many groups. Historical discrimination—like redlining and biased lending practices—means communities of color often face more barriers to building good credit.

And let’s not forget: Credit bureaus are here to serve lenders, not consumers. That’s why fixing errors on your report can feel like pulling teeth, and why the system always seems stacked against you.

The Bottom Line

Credit reporting has come a long way from its gossip-ridden origins, but it’s still not perfect. The system was built to protect lenders, not you, and that’s still obvious today.

So, what can you do? Stay informed. Check your credit reports regularly, dispute mistakes, and know your rights. Because while the system isn’t going anywhere, you don’t have to let it run your life.

Categories

Recent Posts

Managing Broker | License ID: 26476

+1(360) 920-1218 | briddick@agentsinbellingham.com